A debate is bubbling up about the validity of how we measure inflation and whether or not it is, in fact, much higher than reported. Some think exploding home prices are indicative of much higher inflation while others maintain that inflation remains stubbornly low despite incredibly loose monetary policy over the past ten years. Part of this is semantics, and we will get into that first; the definition of inflation just doesn’t encompass some of the things that are exploding in price. There are, however, legitimate complaints about how inflation is measured and further points about what, exactly, we want to understand with inflation.

To get at the heart of the debate, we need to explicitly define inflation because it helps explain most of the disparity between the two camps. As defined in economics, inflation is the rise in the cost of living over time. This happens naturally because there is not a stable quantity of the thing we use to price those goods and services.

More money is created over time both through ‘printing’ by governments and through private lending. The latter deserves its own explanation. As an example, when you buy a house using a mortgage, you are spending money that banks have on deposit from customers. The people who have deposited the money still have that money, but so does the seller of the house. As the supply of money increases, we all have more of it available, which in turn means sellers can charge more for the same thing because the desire for goods and services has not changed. If it all sounds a bit convoluted, don’t worry. It just means that more money exists, so goods and services costs proportionally more. Unfortunately, that is not the end of the story.

Recall that inflation is the rise in costs, not the existence of more money. Previously, it was assumed that there was a somewhat linear relationship between money supply and prices for consumer goods. Over the past decade, the supply of money exploded, but prices of goods stayed relatively stable. In fact, we have had the lowest rates of inflation in modern history as measured by the CPI (consumer price index). It turns out demand for goods and services is driven by consumers, not money supply, and the money was not making its way into the hands of consumers. Instead, it has been stuck in financial markets, which is where prices HAVE exploded. For context, the S&P 500, an index tracking the largest corporations in America, has nearly quadrupled over the past ten years. Meanwhile, the CPI has risen by less than 30%. Median wages have risen by even less than that.

What does it all mean? Real wages, or, put more simply, purchasing power over time, have stagnated. Financial assets have quadrupled. People can buy approximately the same quantities of goods and services, but they have very little access to financial markets. This makes it more difficult to build wealth over time, which will make it more difficult to retire or achieve financial independence. If you were already invested, you’ve probably done quite well. It’s the next generation that will have problems. Millennials will probably have a much more difficult time later in life because the financial markets are unlikely to perform as well over the next 10-20 years.

There’s another problem, too. Extreme levels of sovereign debt (this is true for the US, but it is also true for most European countries, Japan, and even China) are going to make it extremely painful to tighten up monetary policy. If we wanted to take the air out of asset prices, we would also cripple governments everywhere. There is simply no easy way out.

There is one possibility, but it is high-risk. If it goes wrong, we could, in theory, get hyperinflation a la Weimar Republic Germany or, more recently, Venezuela. Hyperinflation is not often seen, but it can utterly destroy an economy. Venezuela went from a middle-income country to one of the most impoverished countries in the world. If we get it right, we could achieve higher growth and the debt would shrink as a percentage of GDP, thus stabilizing the situation. What, you may ask, is this gambit?

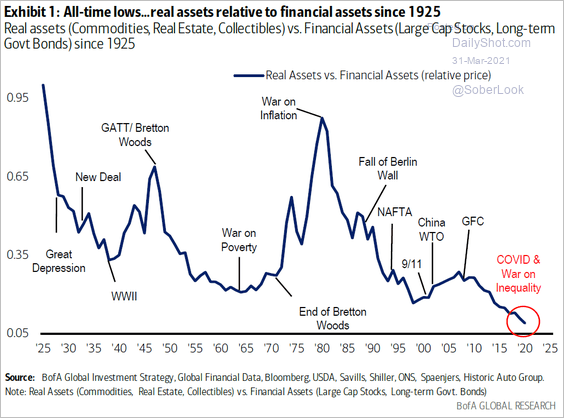

We are seeing it play out right now. Putting as much money into the hands of consumers as possible and making massive investments racks up huge deficits, but it also could result in higher inflation, higher wages, and financial assets falling in terms of median income. To put it mildly, the downsides are catastrophic. However, there are few good options and this offers us, by far, the highest upside. Additionally, assets such as infrastructure and intellectual property offer good value compared to financial assets. Just look at what has happened to real assets (real estate, infrastructure, etc) compared to financial assets (stocks, debt, etc) over time (below). Guessing the odds of each outcome is a fool’s errand, but all signs currently point to the gambit working. GDP growth projections are overwhelmingly positive. The danger is in spending money on things that do not provide real growth, like bailouts of low-productivity companies (cash-eating zombies!) or try to over-regulate, resulting in a quagmire and high inflation without real growth. It’s a thin line, but one we must walk regardless.